What is a Personal Contract Plan?

What is PCP Finance?

Many car dealers are now offering finance in the form of a Personal Contract Plan (PCP) to consumers when they are buying a car. PCPs can appear very attractive because of the low monthly repayments and the convenience of being able to buy your car and sort out your finance in the same place. However, it is important to understand how these products work before you sign any agreements.

Pros

- Low monthly repayments

- Small deposit

- A choice of what to do at end of repayment term

- Quick and easy to arrange

Cons

- Mileage and condition of car affects the costs

- Total amount paid may be more than with hire purchase

- Have to pay the outstanding balance to keep the car

- You don't own the car until the final repayment

How does a PCP work?

A Personal Contract Plan is a type of hire purchase agreement. Under these agreements, you do not own the car until you have made the final repayment.

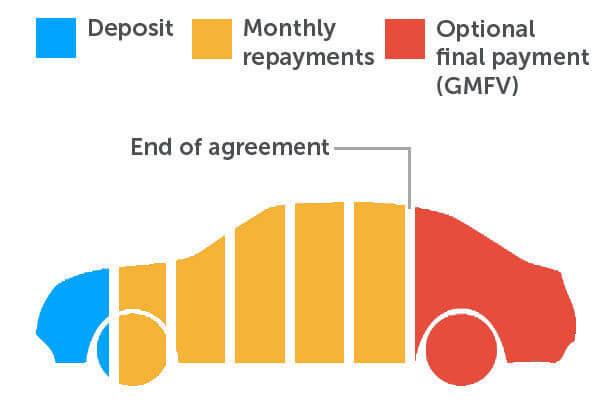

A PCP repayment is broken down into three BASIC parts:

- The Deposit

- Monthly Repayments

- Guaranteed Minimum Future Value (GMFV)

The deposit – a PCP deposit is typically between 10% and 30% of the value of the car. You can pay the deposit in cash or alternatively you can trade in your old car which can reduce the deposit amount down even further.

Monthly repayments - PCP contracts are usually made for terms between three to five years. Under a PCP, monthly repayments are generally quite low compared to a regular finance arrangement.

Guaranteed Minimum Future Value (GMFV) – The GMFV is the balance amount you will have to pay in order to own the car at the end of the agreement. The final payment is based on the estimate of the future value of the at the end of the three to five years. Multiple factors are taken into account when calculating the final payment at the end of the finance term; the car you are buying, the length of the agreement, the condition of the car at the end of the agreement and your annual mileage.

What happens at the end of the agreement?

At the end of the PCP term, there are a number of options you can choose:

- Pay a final payment and keep the car (you pay the guaranteed minimum future value (GMFV) is also more commonly known as a 'balloon payment').

- Hand the car back. By handing the car back, you generally don't have to pay the dealer anything but you may end up having to pay a penalty under the terms of the contract if you have not complied with all the terms and conditions outlined at the beginning of the finance agreement. You also will no longer have the car.

- Put the car down as the deposit on another car and enter into another PCP agreement. The original deposit you put down on the first car will not be given back to you if you use the car as a deposit for a new PCP agreement. The equity you have built up in your monthly repayments and the difference of the GMFV is what you put towards the new car. All you have to put towards the new deposit is whatever equity you built up from the first PCP. This equity may be less than the deposit required for the new PCP, so be aware that you might have to top the deposit up. Be aware, though, that this amount can amount to a couple of thousand euros.

Comparing a PCP with a personal loan

With a personal loan, you borrow the money, pay for your car and you own that car immediately.

Under a PCP agreement, you do not own the car. Essentially you are hiring the car for an agreed period of time, usually 3-5 years.

You can only ever own the car when you make the final repayment. A very important thing to remember when taking out a PCP finance contract, if you were to run into financial difficulty during your PCP agreement period, you cannot sell the car to pay off your debt.

How flexible is a PCP?

Personal Contract Plans are among some of the least flexible forms of finance you can acquire. All repayments are fixed for the term of the agreement so you usually cannot increase your repayments each month if you wish to do so and if you want to extend the term of the agreement, you may be charged a rescheduling fee.

What to watch out for

Before you sign up to a PCP make sure you fully understand the terms and conditions attached to the agreement:

Mileage:

One of the first things you will agree to when you sign up to a PCP is to agree to the number of kilometres you are going to clock up over the period of the agreement. The mileage you clock up on the car has a direct correlation with the GMFV which was agreed to at the beginning of the finance term. If you keep to the agreed mileage, the car will have a guaranteed minimum future value at the end of the agreement. If you exceed the agreed annual mileage you may end up owing more on the final payment. (Remember, even if you were to hand the car back it would still cost you money if you have exceeded the maximum allowed mileage. This is often charged at a set fee per kilometre over the agreed estimate.)

Half rule:

The ‘half rule’ allows you to end a PCP agreement at any time and return your car. It is called the ‘half rule’ because you have to pay half the purchase price. If you have not yet paid half the purchase price you can still return the car but you will owe the difference between the repayments you have made and half the purchase price. If you get into financial difficulty, returning the car using the half rule may be a good option because the finance company may decide to repossess the car if repayments are not met.

Small print:

It is very important to look at the small print. At the beginning of the contract, you will agree to a number of different terms and conditions. An example of these terms and conditions would be the cap on the number of miles/kilometres you are allowed to clock up over the period of the agreement. You may also have to commit to certain car servicing requirements. Always read the small print before you sign up.

Finance options:

Always contrast and compare all the different finance options that you can avail of. It is a good idea to compare the total amount payable on a personal loan (cost of credit) with the PCP cost (the deposit, plus monthly repayments and final payment). Make sure you also compare the terms and conditions of each option.

Fees and charges:

It is advised to always find out any additional fees and charges which can be applied to the contract plan. You are entitled to a list of all additional charges and fees, so ask the garage for this before you sign up to any agreement. Ask if there is any documentation fee for setting up the agreement, missed repayments fees or repossession charges.

How is interest charged?

The rate of interest varies on PCPs depending on the finance company and the type of car you are financing. The interest is calculated at a fixed rate on the total amount of borrowings for each year of the agreement. One of the downsides with PCP’s is, if you pay off the agreement earlier than planned it may work out more expensive than if you had taken out a variable rate personal loan. Another aspect to be aware of is that the deposit you pay at the beginning of the contract will have an impact on the amount of interest you pay.

Can your car be repossessed?

If the terms of the agreement are broken, for example, by missing repayments, your car can be repossessed. If the repayments have been less than one-third of the purchase price, the car finance company can take back your car without taking legal action against you.

If you have paid more than one-third, the lender cannot repossess the car without taking legal action. In addition to this, the car cannot be repossessed from your home, regardless of how much money you’ve paid back.

If your car is repossessed, the finance company will generally sell the car and the money goes towards the outstanding debt, but you will still have to make repayments until the entire debt is paid off.

Can a PCP affect your credit record?

As with other types of credit, the lender is obliged to send details of the repayments you make to a credit-reference agency, such as the Irish Credit Bureau (ICB).

Example of a typical 0% APR PCP repayment schedule

| Price | €20,245 |

| Deposit | €6,074 |

| Monthly repayments (for 36 months) | €196.83 |

| Guaranteed Future Value (final payment) | €7,086 |

(the information contained above is general information and does not intend to be or does not constitute financial advice)

Author

Justin Kavanagh

Justin Kavanagh is a recognised leader

in automotive intelligence and vehicle

data supply to the entire motor industry.

He has almost 20 years experience in

building systems from the ground up.

As the Managing Director of Vehicle

Management System, he understands the

need and importance of trustworthy and

reliable vehicle history and advice to

both the trade and the public.

Follow me on LinkedIn