Are New Car Lenders Victims of Their Own Success?

Are New Car Lenders Victims of Their Own Success?

Dealerships have been busy releasing new cars to customers with attractive car finance deals which are known as Personal Contract Plans.

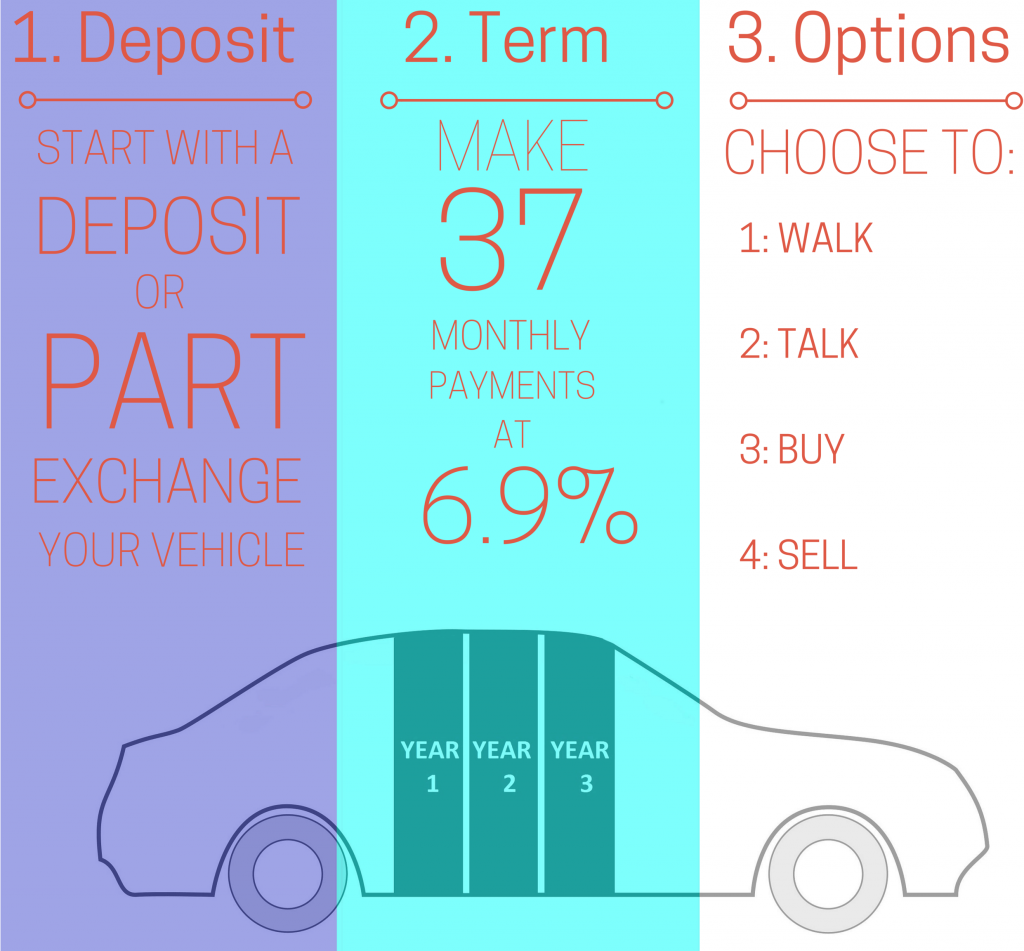

Under these contract plans, the customer puts up part of the money and can drive off in a new car in no time at all.

These payment plans have relatively low monthly repayments compared to other finance arrangements and are agreed as long as the customer meets certain specific requirements under the contract.

One of the stipulations of the contract is a cap on how many miles the car can be driven per year. Another aspect of the contract would be that no damage is done to the vehicle. If these requirements are met, the motor company agrees to pay a guaranteed minimum value for that car in three year's time.

These Personal Payment Plans basically allow the customer to hand back the keys and take up a new deal if they like. They can also pay a bullet payment on the rest of the car.

In banking and finance, these bullet loans allow a payment of the entire principal of the loan and sometimes the principal plus the interest when the payment is due at the end of the loan term. Loans with bullet repayments are also referred to as balloon loans.

The deferral of the principal payments until the loan matures results in lower monthly payments during the life of the loan but this in itself presents a significant risk to the borrower who is not prepared to make the lump sum payment or make other arrangements.

At the end of these terms, most people seem to hand back the keys and go again. It means that they will never actually own the car. As long as they can keep replacing them, they may not care. Some are changing for a new car after just two years.

PCPs have been driving the massive rise in new car sales in Ireland in the last few years. Since 2014 there have been around 360,000 new cars registered in Ireland and many of these have been bought through PCPs.

One concern for the manufacturers going in the short-term is that a glut of second-hand PCP contracted cars which will be hitting the Irish market very shortly. With the greater devaluation of used cars in Ireland since Brexit, they will see a greater drop in the residual value of the cars than first envisioned.

The managing director of Ford Ireland, Ciaran McMahon, recently said that second-hand car values had fallen by around €2,000. Up to 70,000 second-hand cars have been imported into Ireland from the UK this year alone and this has had an effect on used car values. Along with this, tens of thousands of cars bought with PCPs in the last three years are also soon to hit the second-hand market. Car makers could find these PCP cars are not worth as much as they expected.

Supply and demand dictate that the more successful PCPs are, the more second-hand cars will come on the market and therefore, the less they will be worth. This is having the effect of undermining the car companies' and lenders' assumptions about their value.

Undermining assumptions, yes but not necessarily undermining their pockets on a grand scale. Are the car manufacturers overly concerned about their PCP residual value calculations? Probably not? PCP’s only increase their business and attract more customers.

It is looking quite likely that car manufacturers may have made incorrect assumptions in the past few years about the future second-hand value of these cars? Some commentators are saying that they are victims of their own PCP success and could end up taking a financial hit on them? Is this really the case? It is probably not the sob story one would think on first look.

The reality is that the big car manufacturers are far from victims. PCPs may look like a good deal for customers and they can be but from the manufacturer's point of view, PCP’s have been a really nifty way for car makers to finance people to buy their product. For example, internationally, Volkswagen Bank has lent out over €100bn to its customers, so business is good for the car manufacturers and they are not worrying at all, more like laughing all the way to their own private bank.

Author

Justin Kavanagh

Justin Kavanagh is a recognised leader

in automotive intelligence and vehicle

data supply to the entire motor industry.

He has almost 20 years experience in

building systems from the ground up.

As the Managing Director of Vehicle

Management System, he understands the

need and importance of trustworthy and

reliable vehicle history and advice to

both the trade and the public.

Follow me on LinkedIn